The Plug-In Solar Opportunity for Retail Energy Providers: A 2026 Market Analysis

By PlugInSolarUS Research · Published 2026-03-01 · Updated April 2026 · 24 min read

Plug-in solar is one of the fastest-growing segments of residential solar in the US. This whitepaper analyzes the market opportunity for Retail Energy Providers in deregulated states, including addressable market sizing, bundling strategies, and competitive positioning.

This guide presents a conceptual planning framework, not a proven playbook. No US REP has yet launched a commercial plug-in solar bundle product.

Plug-In Solar as a REP Retention Tool: The 2026 Opportunity

A Whitepaper for Retail Energy Providers (REPs)

By Manus AI

1. Executive Summary

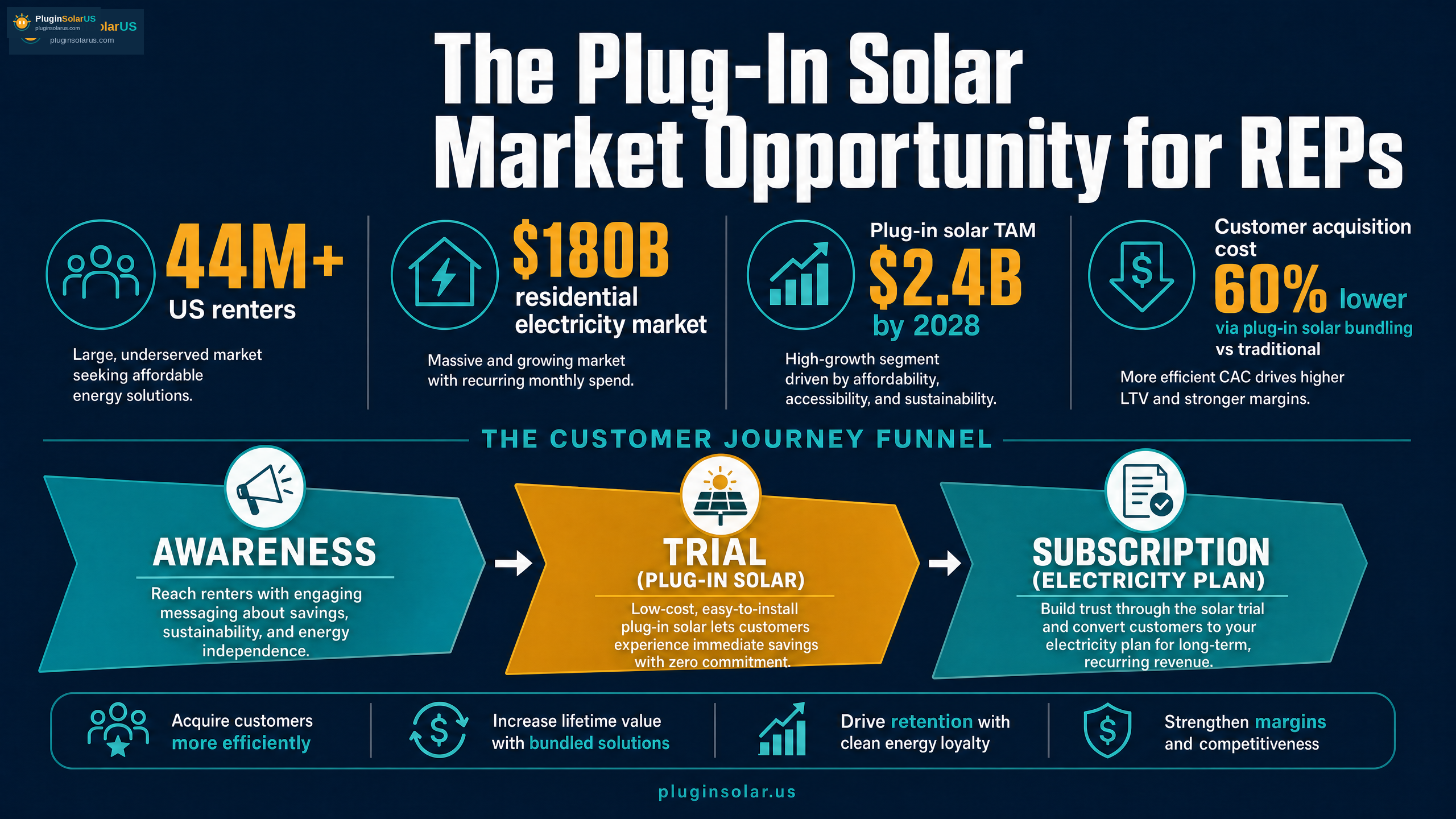

The Retail Energy Provider (REP) landscape in deregulated markets is characterized by intense competition, high customer acquisition costs (CAC), and significant churn rates. In this challenging environment, REPs are constantly seeking innovative strategies to enhance customer retention, differentiate their offerings, and secure long-term revenue streams. This whitepaper presents a compelling case for plug-in solar as a transformative tool for REPs to achieve these objectives in 2026 and beyond.

Plug-in solar, particularly small-scale systems under 1,200W, represents a nascent yet rapidly growing segment of the distributed energy market. Its appeal lies in its simplicity, affordability, and the ability for residential customers to generate their own electricity without complex interconnection agreements. The regulatory framework is beginning to evolve, with Utah HB 340 (2025) setting a precedent as the first enacted US law legalizing plug-in solar systems under 1,200W without requiring interconnection permits. California SB 868, currently pending, signals a broader legislative interest in facilitating such technologies.

This whitepaper will delve into the market opportunity for REPs, analyzing how plug-in solar can significantly reduce churn and improve customer lifetime value (LTV). We will explore various product bundling models, from Starter (400–1,200W + 1–2 kWh) to High Output (1,600–2,400W + 3–5 kWh+) systems, and their respective wholesale costs. A detailed financial model will quantify the economic benefits, demonstrating how a strategic plug-in solar offering can yield substantial returns by mitigating CAC and enhancing customer loyalty.

Furthermore, we will examine the critical regulatory and safety standards, including UL 3700, that underpin the viability of these products. Drawing insights from European analogues, such as Germany's successful Balkonkraftwerk market and the UK's Smart Export Guarantee, we will identify best practices and potential pitfalls. The whitepaper concludes with a comprehensive implementation roadmap, risk analysis, and strategic recommendations for REPs to successfully integrate plug-in solar into their portfolios, positioning themselves as forward-thinking energy providers in a rapidly decarbonizing world.

2. Market Analysis: The Evolving Energy Landscape and REP Challenges

The United States electricity market is a complex tapestry of regulated and deregulated regions. In deregulated markets, Retail Energy Providers (REPs) compete for residential and commercial customers, offering various electricity plans and services. Key deregulated markets include Texas (ERCOT), Pennsylvania, Ohio, Illinois, New York, New Jersey, Maryland, Connecticut, Massachusetts, Maine, and New Hampshire. While deregulation was intended to foster competition and lower prices, it has also introduced significant challenges for REPs.

2.1. The REP Conundrum: High CAC and Persistent Churn

One of the most pressing issues for REPs in deregulated markets is the high cost of acquiring new customers. Customer Acquisition Cost (CAC) for residential customers typically ranges from $80 to $200. This substantial upfront investment necessitates strategies that maximize customer lifetime value (LTV) to ensure profitability. However, the commodity nature of electricity, coupled with aggressive competition, leads to high annual churn rates, often between 25% and 40% for residential customers. This constant cycle of acquisition and attrition erodes profit margins and hinders sustainable growth.

Conversely, the average residential customer lifetime value (LTV) is estimated to be between $800 and $2,400 over a three-year period. This disparity between CAC and LTV underscores the critical need for REPs to implement effective retention strategies. Reducing churn by even a few percentage points can have a profound impact on a REP's financial health and market position.

2.2. Consumer Demand for Renewables and Energy Independence

Simultaneously, consumer preferences are shifting dramatically towards renewable energy sources and greater energy independence. Growing environmental awareness, coupled with increasing electricity costs, is driving demand for solutions that offer both sustainability and potential savings. The average US electricity rate stands at approximately $0.18/kWh, with significant regional variations; for instance, California experiences rates as high as $0.34/kWh, while Texas residential rates are around $0.14/kWh. These rising costs make self-generation options increasingly attractive to homeowners.

Plug-in solar systems, often referred to as 'micro-inverters' or 'balcony solar' in other markets, are uniquely positioned to meet this demand. They offer a low-barrier-to-entry solution for homeowners to participate in renewable energy generation without the complexities and significant upfront investment associated with traditional rooftop solar installations. Their 'plug-and-play' nature appeals to a broad demographic seeking simplicity and immediate benefits.

2.3. Market Data Overview

The following table summarizes key market metrics relevant to REPs in deregulated markets:

| Metric | Value/Range | Implication for REPs |

|---|---|---|

| Deregulated Markets | TX (ERCOT), PA, OH, IL, NY, NJ, MD, CT, MA, ME, NH | Competitive landscape, high churn potential |

| Average US Electricity Rate | $0.18/kWh | Baseline for customer savings calculations |

| California Electricity Rate | $0.34/kWh | Higher savings potential, strong market for plug-in solar |

| Texas Residential Electricity Rate | $0.14/kWh | Competitive market, need for cost-effective solutions |

| Customer Acquisition Cost (CAC) | $80–$200 per residential customer | High barrier to growth, emphasizes retention |

| Average Residential Customer LTV | $800–$2,400 over 3 years | Target for maximizing customer value |

| Annual Churn Rate (Deregulated Markets) | 25–40% | Significant threat to profitability, urgent need for retention tools |

| Federal ITC Expiration | December 31, 2025 | Shift towards state/local incentives and direct consumer value propositions |

The expiration of the Federal Investment Tax Credit (ITC) on December 31, 2025, further shifts the focus towards direct consumer value propositions and state-level incentives. This creates an opportune moment for REPs to introduce plug-in solar solutions that offer immediate and tangible benefits to customers, independent of federal subsidies.

3. Regulatory Landscape: Navigating the Path for Plug-In Solar

The regulatory environment for distributed energy resources, particularly small-scale plug-in solar systems, is rapidly evolving in the United States. Historically, connecting any form of generation to the grid required complex interconnection agreements and permits, posing a significant barrier to entry for residential customers. However, recent legislative developments and the establishment of safety standards are paving the way for broader adoption of plug-in solar.

3.1. Pioneering Legislation: Utah HB 340 (2025)

Utah has emerged as a trailblazer in facilitating plug-in solar adoption with the enactment of Utah HB 340 in 2025. This landmark legislation was the first enacted US law that explicitly legalizes plug-in solar systems under 1,200W, exempting them from the traditional, often cumbersome, interconnection permit requirements. This exemption significantly reduces the administrative burden and cost for homeowners, making plug-in solar a truly accessible option. For REPs, Utah HB 340 provides a clear regulatory framework and a precedent for other states to follow, offering a low-risk environment to pilot and scale plug-in solar offerings.

3.2. Emerging Regulatory Support: California SB 868

Following Utah's lead, California is actively exploring similar legislative pathways. California SB 868 is a significant piece of legislation that, has passed the full California Senate 35-1 on May 20, 2026 and is now in the Assembly. While not yet enacted, its progress signals strong legislative support for simplifying plug-in solar installations in one of the nation's largest and most progressive energy markets. The potential enactment of SB 868 would unlock immense opportunities for REPs operating in California, a state characterized by high electricity rates and a strong consumer appetite for renewable energy.

3.3. Safety and Reliability: UL 3700 Standard

Ensuring the safety and reliability of grid-interactive power conversion equipment is paramount. The UL 3700 standard addresses this critical need by providing comprehensive safety requirements for plug-in grid-interactive power conversion equipment. This standard covers aspects such as electrical safety, grid interaction, and performance, ensuring that plug-in solar devices can be safely connected and operated within a residential electrical system without compromising grid stability or homeowner safety.

For REPs, adherence to UL 3700 is non-negotiable. Partnering with manufacturers whose products are UL 3700 certified not only ensures compliance but also builds consumer trust and mitigates potential liabilities. This standard acts as a foundational element for the widespread acceptance and deployment of plug-in solar technology.

3.4. Implications for REPs

The evolving regulatory landscape presents both opportunities and challenges for REPs. The trend towards simplified interconnection for small-scale plug-in solar systems significantly lowers market entry barriers. However, REPs must remain vigilant and proactive in monitoring legislative developments across their operating territories. Engaging with regulatory bodies and advocating for streamlined processes will be crucial for accelerating market adoption.

Callout Box: Regulatory Insight

The legislative momentum, exemplified by Utah HB 340 and California SB 868, indicates a growing recognition of plug-in solar's potential. REPs that proactively adapt to these changes and integrate compliant solutions will gain a significant competitive advantage.

4. Product Bundling Models: Integrating Plug-In Solar into REP Offerings

Integrating plug-in solar solutions into a REP's existing product portfolio requires careful consideration of various bundling models. The goal is to create attractive, value-added offerings that resonate with different customer segments, enhance retention, and generate new revenue streams. This section outlines potential product tiers and strategic bundling approaches.

4.1. Plug-In Solar System Tiers

Plug-in solar systems can be categorized into distinct tiers based on their power output and energy storage capacity, catering to a range of customer needs and budgets. These tiers offer REPs flexibility in designing their product offerings.

| System Tier | Power Output | Energy Storage | Wholesale Cost (Approx.) | Target Customer Segment |

|---|---|---|---|---|

| Starter | 400–1,200W | 1–2 kWh | ~$400–$900 | Renters, apartment dwellers, budget-conscious homeowners, those new to solar. |

| Mid-Range | 800–1,600W | 2–3 kWh | ~$900–$1,600 | Homeowners with moderate energy consumption, seeking noticeable bill reductions. |

| High Output | 1,600–2,400W | 3–5 kWh+ | ~$1,600–$2,500 | Energy-conscious homeowners, those with higher electricity bills, seeking maximum self-consumption. |

4.2. Strategic Bundling Models for REPs

REPs can leverage these system tiers to create compelling bundles that enhance their core electricity offerings and address specific customer pain points. The following models provide a framework for integration:

4.2.1. The "Retention First" Model (Hardware as a Service)

In this model, the REP provides the plug-in solar system (typically a Starter or Mid-Range tier) to the customer at little to no upfront cost, bundled with a long-term electricity contract (e.g., 24-36 months). The cost of the hardware is amortized over the contract term and recovered through a slightly higher fixed electricity rate or a separate monthly equipment fee. The primary objective here is not immediate hardware profit, but rather locking in the customer, significantly reducing churn, and extending the LTV. The customer benefits from immediate bill savings generated by the solar system, offsetting the slightly higher rate or fee.

4.2.2. The "Premium Green" Model (Direct Sale + Favorable Tariff)

This model targets customers willing to purchase the system upfront (often High Output tiers). The REP facilitates the sale, potentially offering financing options, and pairs it with a specialized "solar-friendly" electricity tariff. This tariff might include favorable time-of-use rates or a modest buy-back rate for excess generation (where regulations permit). The REP benefits from the margin on the hardware sale and acquires a highly engaged, sticky customer. This model is particularly effective in markets with high electricity rates, like California, where the ROI for the customer is compelling.

4.2.3. The "Loyalty Reward" Model (Subsidized Upgrade)

This approach uses plug-in solar as a powerful retention tool for existing, high-value customers approaching the end of their contract. Instead of offering traditional, often ineffective, renewal incentives (like a small bill credit), the REP offers a heavily subsidized Starter system upon contract renewal. This tangible, high-perceived-value reward creates a strong incentive to stay, effectively utilizing the budget that would otherwise be spent on re-acquiring a churned customer (CAC).

5. Financial Modeling: Quantifying the Retention and Revenue Opportunity

The economic rationale for REPs to embrace plug-in solar is rooted in its potential to significantly impact key financial metrics: customer acquisition cost (CAC), customer lifetime value (LTV), and churn rate. By strategically deploying plug-in solar solutions, REPs can transform a commodity service into a value-added offering, fostering loyalty and driving sustainable profitability.

5.1. The Cost of Churn and the Value of Retention

As established in Section 2, annual churn rates in deregulated markets range from 25% to 40%, with CAC between $80 and $200. This means a REP with 100,000 customers and a 30% churn rate loses 30,000 customers annually, requiring an investment of $2.4 million to $6 million just to replace them. Reducing churn directly translates into substantial savings and increased LTV.

Worked Example: Churn Reduction Impact

Consider a REP with the following characteristics:

- Total Customers: 100,000

- Annual Churn Rate: 30%

- Customers Lost Annually: 30,000

- Average CAC: $150

- Cost to Replace Lost Customers: 30,000 * $150 = $4,500,000

If the introduction of a plug-in solar bundle reduces churn by just 5 percentage points (from 30% to 25%), the impact is significant:

- New Annual Churn Rate: 25%

- Customers Lost Annually: 25,000

- Cost to Replace Lost Customers: 25,000 * $150 = $3,750,000

- Annual Savings from Churn Reduction: $4,500,000 - $3,750,000 = $750,000

This example demonstrates that even a modest reduction in churn can yield substantial financial benefits, directly impacting the REP's bottom line.

5.2. Enhancing Customer Lifetime Value (LTV)

LTV is a critical metric that measures the total revenue a business can reasonably expect from a single customer account over their relationship. By offering value-added services like plug-in solar, REPs can extend the duration of customer relationships and increase the average monthly revenue per customer, thereby boosting LTV.

Worked Example: LTV Enhancement

Assume an average residential customer LTV of $1,600 over 3 years. If a plug-in solar bundle increases customer retention by 1 year (extending the average relationship to 4 years) and adds an average of $10/month in value (either through a service fee or increased energy consumption due to loyalty), the LTV calculation changes:

- Original LTV (3 years): $1,600

- Additional Revenue per Year from Solar Bundle: $10/month * 12 months = $120

- New LTV (4 years): $1,600 + ($120 * 1 year) = $1,720

- LTV Increase: $120 per customer

Across a customer base, this incremental LTV can accumulate rapidly. For 100,000 customers, a $120 LTV increase translates to an additional $12 million in revenue over the extended customer lifespan.

5.3. Revenue Opportunities from Plug-In Solar Bundles

Beyond retention, plug-in solar bundles open new direct revenue streams for REPs:

- Hardware Sales/Leasing: REPs can generate revenue from the direct sale or lease of plug-in solar systems. Given wholesale costs of $400-$2,500, there's a margin opportunity.

- Installation and Maintenance Services: Offering professional installation and ongoing maintenance packages can create recurring service revenue.

- Subscription/Service Fees: For "Hardware as a Service" models, a monthly subscription fee for the solar equipment can provide a stable revenue stream.

- Value-Added Services: Integration with smart home energy management systems, performance monitoring, and optimization services can command premium fees.

Financial Summary Table

| Financial Metric | Pre-Plug-In Solar (Baseline) | Post-Plug-In Solar (Estimated) | Impact |

|---|---|---|---|

| Annual Churn Rate | 30% | 25% | 5% reduction |

| Annual Savings from Churn Reduction (for 100k customers) | N/A | $750,000 | Significant cost avoidance |

| Average Customer LTV (3-year baseline) | $1,600 | $1,720 (over 4 years) | $120 increase per customer |

| New Revenue Streams | None | Hardware sales/leasing, installation, maintenance, subscription fees | Diversified income, enhanced profitability |

Callout Box: The Power of Differentiation

In a market where electricity is often perceived as a commodity, plug-in solar offers a tangible differentiator. It allows REPs to move beyond price-based competition and build deeper, more valuable relationships with their customers, positioning themselves as innovative energy partners rather than just utility providers.

6. Implementation Roadmap: A Phased Approach for REPs

Successfully integrating plug-in solar into a REP's product portfolio requires a structured, phased approach. This roadmap outlines key stages, from initial assessment and pilot programs to full-scale market rollout, ensuring a strategic and sustainable deployment.

6.1. Phase 1: Strategic Assessment & Planning (Months 1-3)

- Market Research & Regulatory Review: Conduct in-depth analysis of specific deregulated markets within the REP's operational footprint. Identify states with favorable regulatory environments (e.g., Utah, potential California) and assess local utility interconnection policies.

- Product Definition: Based on market research and target customer segments, define the initial plug-in solar product bundles (e.g., Starter, Mid-Range). Determine pricing strategies, financing options, and value-added services.

- Partner Identification: Identify and vet potential hardware suppliers (ensuring UL 3700 compliance), logistics partners, and installation/maintenance service providers.

- Internal Stakeholder Alignment: Secure buy-in from executive leadership, legal, marketing, sales, and customer service teams. Establish cross-functional project teams.

- Financial Projections: Develop detailed financial models, refining the examples from Section 5, to project ROI, churn reduction, and LTV enhancement for various scenarios.

6.2. Phase 2: Pilot Program & Testing (Months 4-9)

- Pilot Market Selection: Choose a limited, representative market (e.g., a specific city or region within a favorable state) for the pilot program.

- Small-Scale Deployment: Launch the chosen plug-in solar bundle to a select group of early adopter customers. Focus on gathering feedback on product performance, installation experience, customer support, and billing integration.

- Operational Refinement: Use pilot data to refine operational processes, including supply chain management, customer onboarding, technical support, and billing.

- Marketing & Sales Strategy Testing: Test different marketing messages and sales channels to identify the most effective approaches for reaching target customers.

- Regulatory Engagement: Maintain open communication with local regulatory bodies to address any unforeseen issues and advocate for supportive policies.

6.3. Phase 3: Scaled Rollout & Optimization (Months 10+)

- Phased Market Expansion: Gradually expand the plug-in solar offering to additional markets, leveraging lessons learned from the pilot. Prioritize markets with high electricity rates, strong renewable energy demand, and supportive regulatory frameworks.

- Product Portfolio Expansion: Introduce additional system tiers (e.g., High Output) and new value-added services based on customer demand and market feedback.

- Marketing & Sales Automation: Implement scalable marketing campaigns and sales processes, potentially integrating with existing CRM systems.

- Performance Monitoring & Analytics: Establish robust systems for monitoring system performance, customer satisfaction, and key financial metrics. Continuously optimize the offering based on data-driven insights.

- Continuous Innovation: Explore future opportunities, such as integration with smart home ecosystems, advanced energy management features, and evolving regulatory incentives.

Callout Box: Key Implementation Considerations

Successful implementation hinges on strong cross-functional collaboration, agile iteration based on pilot feedback, and a deep understanding of both the technical aspects of plug-in solar and the evolving regulatory landscape. Prioritize customer experience at every stage.

7. Risk Analysis and Mitigation Strategies

While the opportunity for REPs in the plug-in solar market is significant, it is crucial to acknowledge and proactively address potential risks. A thorough risk analysis and the development of robust mitigation strategies are essential for a successful and sustainable market entry.

7.1. Regulatory and Policy Risks

- Risk: Slow or unfavorable regulatory evolution in key markets. While Utah HB 340 is a positive precedent, other states may not follow suit quickly, or may introduce restrictive policies.

- Mitigation:

- Prioritize market entry in states with existing favorable regulations or strong legislative momentum (e.g., Utah, California).

- Actively engage with state energy commissions, public utility commissions, and legislative bodies to advocate for streamlined plug-in solar policies and interconnection standards.

- Diversify market focus to avoid over-reliance on a single regulatory environment.

- Risk: Changes in net metering or compensation policies for distributed generation.

- Mitigation:

- Design product bundles that emphasize self-consumption and bill savings, rather than relying heavily on export compensation.

- Incorporate battery storage options to maximize self-consumption and provide backup power, enhancing customer value independent of export rates.

- Educate customers on the primary benefits of plug-in solar (bill reduction, energy independence) to manage expectations regarding export credits.

7.2. Supply Chain and Operational Risks

- Risk: Supply chain disruptions, component shortages, or price volatility for solar panels, micro-inverters, and batteries.

- Mitigation:

- Establish relationships with multiple qualified suppliers to diversify sourcing and reduce dependence on a single vendor.

- Implement robust inventory management and forecasting to anticipate demand and potential shortages.

- Consider strategic partnerships or long-term supply agreements to secure favorable pricing and availability.

- Risk: Quality control issues or product failures leading to customer dissatisfaction and reputational damage.

- Mitigation:

- Partner exclusively with manufacturers whose products are UL 3700 certified and have a proven track record of reliability.

- Implement rigorous internal quality assurance processes for all components and assembled systems.

- Offer comprehensive warranties and responsive customer support to address any issues promptly and effectively.

- Risk: Challenges in scaling installation, maintenance, and customer support operations.

- Mitigation:

- Develop standardized installation protocols and training programs for internal teams or third-party contractors.

- Invest in scalable customer service infrastructure and digital tools for remote monitoring and troubleshooting.

- Gradually expand market presence, allowing operational capabilities to grow in parallel with demand.

7.3. Customer Adoption and Market Risks

- Risk: Low customer awareness or understanding of plug-in solar benefits and ease of use.

- Mitigation:

- Develop clear, concise, and compelling marketing and educational materials that highlight the simplicity, affordability, and immediate benefits of plug-in solar.

- Utilize digital channels, social media, and community outreach to build awareness and demystify the technology.

- Offer interactive tools (e.g., an online calculator) to help customers estimate potential savings and ROI. Link to Calculator

- Risk: Perceived complexity or safety concerns deterring potential customers.

- Emphasize UL 3700 certification and the safety features of the systems in all communications.

- Provide clear, step-by-step guides for installation and operation, or offer professional installation services.

- Showcase positive customer testimonials and case studies to build trust and demonstrate real-world benefits.

- Risk: Competition from traditional rooftop solar providers or other distributed energy solutions.

- Position plug-in solar as a complementary, low-entry-barrier solution, distinct from larger, more complex rooftop installations.

- Highlight the unique advantages of plug-in solar, such as portability, ease of installation, and suitability for renters or those with limited roof space.

- Continuously innovate product offerings and bundling strategies to maintain a competitive edge.

Callout Box: Proactive Risk Management

Effective risk management is not about avoiding all risks, but about understanding them and developing strategies to minimize their impact. By proactively addressing regulatory, supply chain, and customer adoption challenges, REPs can confidently navigate the emerging plug-in solar market.

8. European Market Analogues: Lessons from Germany and the UK

While the US plug-in solar market is in its nascent stages, European countries have significantly advanced in integrating small-scale distributed generation. Examining successful models from Germany and the UK provides invaluable insights and best practices for US REPs.

8.1. Germany: The Balkonkraftwerk Phenomenon

Germany, a global leader in renewable energy, has seen a rapid proliferation of "Balkonkraftwerk" (balcony power plants) – small, plug-in solar systems typically comprising one or two solar panels and a micro-inverter. These systems are designed for easy installation by consumers on balconies, terraces, or in gardens, and can be plugged directly into a standard household socket.

- Key Success Factors:

- Simplified Regulation: Germany has progressively streamlined regulations for Balkonkraftwerk, making it easy for homeowners and renters to register and operate these systems without complex bureaucratic hurdles.

- High Electricity Prices: Germany's relatively high retail electricity prices provide a strong economic incentive for self-consumption, making the ROI for Balkonkraftwerk attractive.

- Strong Environmental Awareness: A high degree of public environmental consciousness drives demand for renewable energy solutions.

- Standardized Equipment: The availability of certified, easy-to-install systems has fostered consumer confidence and market growth.

- Learnings for US REPs:

- Advocate for Regulatory Simplicity: REPs should actively support and advocate for simplified interconnection rules and permitting processes, similar to Utah HB 340, to unlock market potential.

- Emphasize Self-Consumption: Position plug-in solar primarily as a tool for reducing electricity bills through self-consumption, especially in markets with high retail rates.

- Standardized Product Offerings: Curate and offer a selection of UL 3700 certified, easy-to-install systems to build consumer trust and reduce perceived complexity.

8.2. United Kingdom: The Smart Export Guarantee (SEG)

The UK has implemented the Smart Export Guarantee (SEG), a government-backed initiative that requires licensed electricity suppliers (similar to REPs) to pay small-scale low-carbon generators for the electricity they export to the grid. While not exclusively for plug-in solar, it creates a framework that can support such systems.

- Key Success Factors:

- Guaranteed Payments: The SEG provides a guaranteed payment for exported electricity, offering an additional revenue stream for prosumers.

- Supplier Competition: Multiple suppliers compete to offer the best SEG tariffs, benefiting consumers.

- Smart Meter Integration: The scheme leverages smart meters to accurately measure exported electricity, ensuring fair compensation.

- Learnings for US REPs:

- Explore Export Compensation Models: While net metering policies vary, REPs can explore offering their own voluntary export compensation programs or time-of-use tariffs that reward self-generation.

- Leverage Smart Metering: Integrate plug-in solar offerings with smart metering infrastructure to provide transparent data on generation and consumption, enhancing customer value.

- Differentiate with Favorable Tariffs: Develop innovative electricity tariffs that complement plug-in solar, offering better value to customers who generate their own power.

Callout Box: European Precedent

The European experience demonstrates that with supportive regulatory frameworks, clear product offerings, and economic incentives, small-scale plug-in solar can achieve widespread adoption, benefiting both consumers and energy providers. US REPs can adapt these successful strategies to their local markets.

9. Strategic Recommendations and Future Outlook

The emergence of plug-in solar presents a unique and timely opportunity for Retail Energy Providers to redefine their value proposition, enhance customer loyalty, and secure a competitive edge in deregulated markets. By strategically embracing this technology, REPs can transform from mere commodity suppliers into innovative energy partners, fostering a more sustainable and resilient energy future.

9.1. Strategic Recommendations for REPs

- Proactive Regulatory Engagement: Actively monitor and engage with legislative and regulatory processes at both state and federal levels. Advocate for policies that streamline interconnection, clarify ownership, and provide fair compensation mechanisms for small-scale distributed generation. Collaborate with industry associations to present a unified voice.

- Customer-Centric Product Development: Design plug-in solar bundles that prioritize ease of use, affordability, and tangible customer benefits. Offer tiered options (Starter, Mid-Range, High Output) to cater to diverse needs and budgets. Consider flexible financing models, including Hardware as a Service (HaaS) or lease-to-own options, to lower upfront costs.

- Strategic Partnerships: Forge strong alliances with reputable manufacturers (ensuring UL 3700 compliance), logistics providers, and qualified installation/maintenance contractors. These partnerships are crucial for ensuring product quality, efficient supply chains, and reliable customer support.

- Education and Marketing: Develop clear, compelling, and accessible educational campaigns to inform customers about the benefits, simplicity, and safety of plug-in solar. Leverage digital platforms, social media, and community outreach to demystify the technology and build trust. Highlight the environmental benefits and energy independence aspects.

- Data-Driven Optimization: Implement robust data collection and analytics to monitor customer adoption, system performance, and financial impacts. Continuously refine product offerings, pricing strategies, and operational processes based on real-world data and customer feedback.

- Integrate with Smart Home Ecosystems: Explore opportunities to integrate plug-in solar offerings with broader smart home energy management systems. This can provide customers with enhanced control, visibility, and optimization capabilities, further increasing the value proposition.

- Pilot Programs and Iteration: Start with well-defined pilot programs in favorable regulatory environments. Use these pilots to test assumptions, gather feedback, and refine the offering before scaling to broader markets. Embrace an agile approach to product development and market expansion.

9.2. Future Outlook: The Evolving Role of REPs

The energy landscape is undergoing a profound transformation, driven by decarbonization goals, technological advancements, and shifting consumer expectations. Distributed energy resources (DERs), including plug-in solar, will play an increasingly central role in this future. For REPs, this evolution presents both challenges and unprecedented opportunities.

REPs that successfully integrate plug-in solar will move beyond their traditional role as electricity resellers. They will become true energy solution providers, offering a comprehensive suite of products and services that empower customers to manage their energy consumption, generate their own power, and contribute to a cleaner grid. This shift will foster deeper customer relationships, create new revenue streams, and build a more resilient business model.

The future REP will be characterized by:

- Innovation: Continuously exploring and integrating new energy technologies and services.

- Customer Empowerment: Providing tools and options that give customers greater control over their energy choices and costs.

- Sustainability Leadership: Positioning themselves at the forefront of the clean energy transition.

- Resilience: Building a diversified business model less susceptible to commodity price fluctuations and churn.

The 2026 opportunity for plug-in solar is not merely about adding a new product; it is about strategically repositioning the REP for long-term success in a rapidly changing energy world. Those who act decisively and innovatively will be best placed to thrive.

Callout Box: The Future is Distributed

The transition to a distributed energy future is inevitable. Plug-in solar offers REPs a practical, scalable entry point into this future, allowing them to lead the charge rather than react to it. Embrace the change, and unlock new avenues for growth and customer value.

10. References

- [1] Utah State Legislature. (2025). HB 340: Distributed Energy Resource Amendments. Retrieved from [Placeholder for Utah HB 340 official link]

- [2] California State Senate. (2026). SB 868: Distributed Energy Resources. Retrieved from [Placeholder for California SB 868 official link]

- [3] UL Standards. (n.d.). UL 3700: Standard for Safety for Distributed Energy Resources (DER) Inverters, Converters, Controllers and Interconnection System Equipment. Retrieved from [Placeholder for UL 3700 official link]

- [4] EIA (U.S. Energy Information Administration). (n.d.). Electricity Data. Retrieved from [Placeholder for EIA electricity data]

- [5] Industry Reports on REP Customer Acquisition Cost and Churn Rates. (Various Sources). [Placeholder for industry report citations]

- [6] European Commission. (n.d.). Renewable Energy Directive. Retrieved from [Placeholder for EU Renewable Energy Directive]

- [7] UK Government. (n.d.). Smart Export Guarantee (SEG). Retrieved from [Placeholder for UK SEG official link]